The SEC announced the adoption of its new pay for performance rules, or Item 402(v) on August 25, 2022. A detailed summary of the new rules can be found within our Alert found here. However, the intent of this shorter brief is to summarize the different approaches for the re-valuation of employee stock options as of either the end of the fiscal year or on the vest date.

For public companies that grant stock options, your main challenge will be developing an expected life for an option that is no longer at the money. We provide some guidance for how to do so below. It’s important to start compiling these historical valuations sooner rather than later, as the initial work to set this up for the first year will be significant. Also, while the new rules only impact public companies, companies planning for an IPO will want to pay attention to these approaches too.

As a reminder, the new rules require all outstanding and unvested awards to be re-valued as of the end of the fiscal year and awards that vest during the fiscal year to be valued on their vest date. The incremental change in fair value from the end of the fiscal year (or vest date if sooner) as compared to the end of the prior fiscal year, is included as Compensation Actually Paid during the year. The guidance states “(3) Fair value amounts must be computed in a manner consistent with the fair value methodology used to account for share-based payments in the registrant’s financial statements under generally accepted accounting principles”. Therefore, it is critical to use a consistent process for pay for performance re-valuation to what was done on the grant date and disclosed in current financial reporting.

Choosing the Appropriate Option Pricing Model

The first consideration in developing these valuations is the appropriate option pricing model to apply. The most prevalent model for valuing plain-vanilla stock options is the Black-Scholes model (with some limited companies disclosing a binomial or a lattice model). Although it is more complex to develop the exercise behavior / expected life assumption for options that are no longer “at-the-money”, we believe that the Black-Scholes model continues to be appropriate for these re-valuations (unless your organization has already switched to a binomial or lattice model prior).

With respect to the assumptions that are used within the Black-Scholes model, it is straightforward to follow a consistent process for estimating expected volatility, expected dividend yield, and the risk-free rate of return.

However, the most significant challenge is to develop an appropriate assumption for the expected life that would be used within the Black-Scholes model. Some of the reasons that it is challenging to develop an expected life for these awards:

- There will be many awards to be valued, each with different levels of “in-the-moneyness”. While some may be in-the-money, others may be underwater. It has been shown that the duration of an option’s expected life is strongly affected by the in-the-moneyness level.

- There will be many awards that have different remaining contractual terms and awards with an earlier contractual term would be expected to be exercised earlier.

Below we have summarized four (4) methodologies that we believe are reasonable approaches to calculate the expected life of an option, and compliant with generally accepted accounting practices.

The determination of exercise behavior and the fair value of employee stock options is one of the more challenging aspects of ASC 718 and calculating Compensation Actually Paid. We have laid out 4 alternatives to consider in developing these valuations.

| Approach 1: The “Midpoint” Approach – This approach under the SEC Staff Accounting Bulletin #107 is the simplest out of the four approaches because it takes the midpoint of the weighted average time-to-vest and the full contractual term. Many companies already use this approach for valuing awards at their grant date. However, the guidance states that this safe harbor calculation should only be allowed for “plain-vanilla” at-the-money options, while it is likely that the option will no longer be at-the-money on the re-valuation at the end of the fiscal year and vest date. Update as of 9/27/2023: Although Infinite Equity believes this to be a “reasonable” approach, Question 128D.21 of the new Compliance & Disclosure Interpretations (C&DI’s) released on 9/27/2023 referenced this approach and it is likely not allowable for purposes of these re-valuations. | Example: An option is granted on March 3, 2020 with a vest date of 3/3/2023 and a 10-year contractual term with an exercise price of $10. The volatility is 60%, a 3% Risk-Free Rate of Return, and no dividend yield. On 12/31/2022, the stock price is $25. As of 12/31/2022, the fair value is: Remaining time to vest = 0.17 years Remaining contractual term = 7.17 years Expected Life = 0.17+ 7.172 = 3.67 years Fair Value = $17.62 |

| Approach 2: IRS Revenue Procedure 98-34 – this revenue procedure sets forth a methodology to value certain compensatory stock options. The expected life in this approach is referred to as the “Computed Expected Life.” The computed expected life is calculated by obtaining the weighted-average expected life of the options and then dividing that by the number of years from the grant date to the expiration date (contractual term). Lastly, multiply the answer from step two by the remaining maximum term. This approach is also widely used by companies in their Proxy for generating estimated payments at the time of termination. | Example (using the same scenario used above, and the original grant date expected life is 6.50 years): Contractual Term = 10 years Remaining Maximum Term = 7.17 years Expected Life = 6.510 x 7.17 = 4.66 years Fair Value = $18.28 |

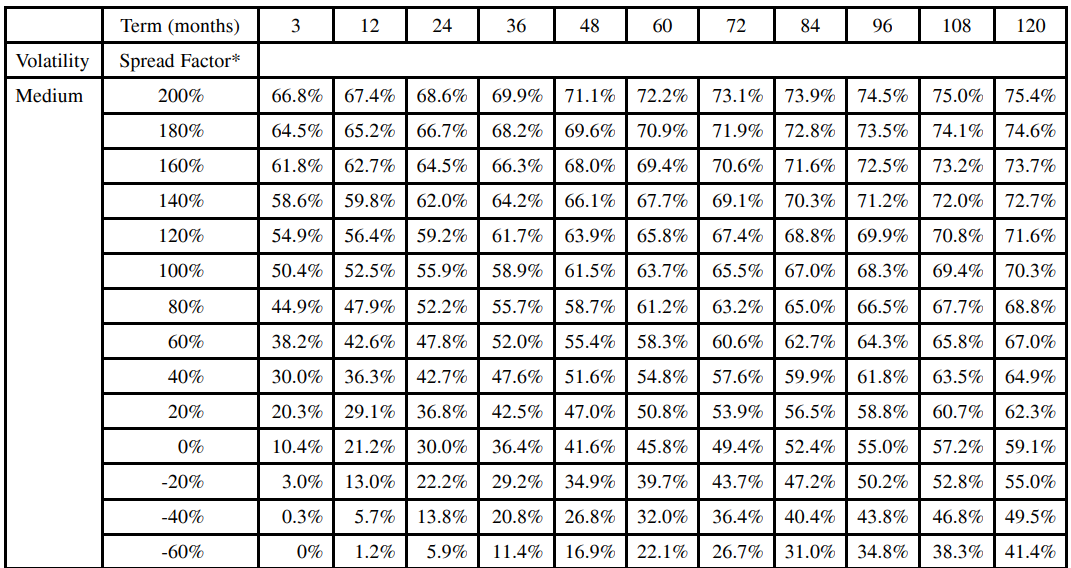

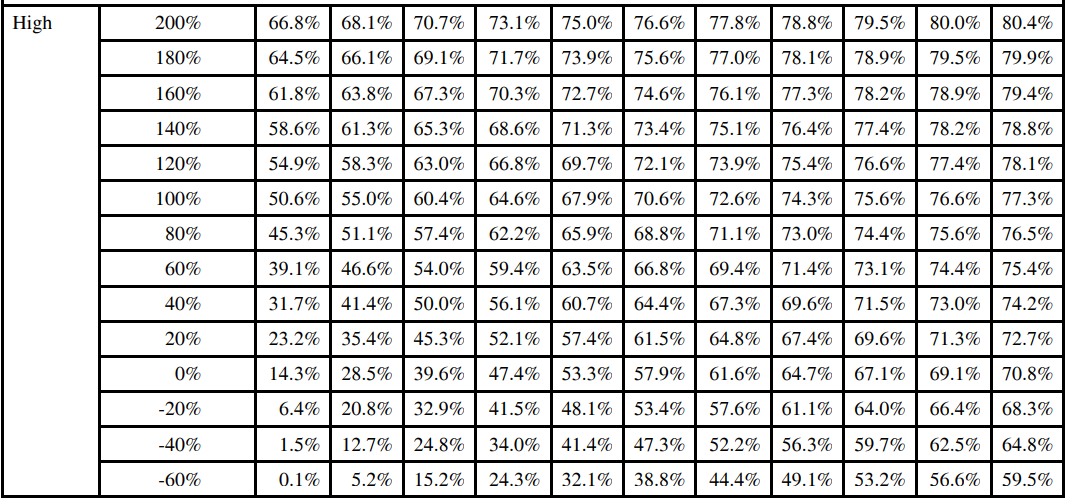

| Approach 3: IRS Revenue Procedure 2003-68 – This revenue procedure provides guidance on the valuation of stock options solely for purposes of §§ 280G and 4999 of the Internal Revenue Code. The term of the option is the number of full months between the valuation date and the latest date on which the option will expire. The benefit of these Safe Harbor tables are that they value stock options as a function of both “moneyness” and “time”. Full tables for Low, Medium, and High volatilities can be found in Appendix 1. | Example (same as prior): Expected Term = 7.17 years x 12 = 86.04 (84 months) Spread: $25/$10-1=150% Final Valuation Factor: 70.3% Fair Value: 70.3% x $25 = $17.58 |

Approach 4: Elapsed Time (Added on 9/27/23) The Elapsed Time approach is an addendum to our prior publication, and only added because it was referenced by the SEC in Question 128D.21 of the C&DI’s released on 9/27/2023. The “elapsed time” approach is not an allowable approach for the re-valuation of employee stock options. | Example: An option is granted on March 3, 2020 with a vest date of 3/3/2023 and a 10-year contractual term with an exercise price of $10. The original expected life is 6.25 years. As of 12/31/2022, the fair value is: Remaining contractual term = 7.17 years Elapsed Time since grant = 2.83 years Expected Life = 6.25 – 2.83 = 3.42 years Fair Value = $17.45 |

The determination of exercise behavior and the fair value of employee stock options is one of the more challenging aspects of ASC 718 and calculating Compensation Actually Paid. We have laid out several alternatives to consider in developing these valuations.

We believe that each of the above approaches are compliant under generally accepted accounting practices. Further, each of these approaches are easily scalable and can be incorporated into the financial reporting systems of equity administrative systems.

Infinite Equity continues to examine the new pay for performance rules and how they will impact both the executive and equity compensation community. For more information on the new pay for performance regulations or assistance navigating these changes, reach out to us at Infinite Equity for help.

Appendix: Safe Harbor Valuation Models from Revenue Procedure 2003-68 for Low, Medium, and High Volatility

The New Rules of Pay Versus Performance